The Guide to Enterprise Management Incentive (EMI) Schemes

Enterprise management incentive (EMI) schemes are one of the most popular ways for companies to distribute equity to employees in the UK. EMI is specifically designed for UK-based startups that are still in the early stages of their development, but which have big ambitions.

In this guide, find out how EMI options work, who can use them, and the benefits and drawbacks of EMIs compared to other employee share schemes.

What are Enterprise Management Incentives (EMIs)?

{{callout-1}}

The Enterprise Management Incentive (EMI) is a type of government-approved, tax-advantaged employee share scheme for companies with a permanent UK base. EMI options are the share options granted by companies under the scheme.

EMI schemes are approved by HMRC, the UK government tax authority. The approval process validates the company's valuation as fair, and confirms the strike price that employees will pay to turn their share options into shares.

When companies set up EMI schemes, employees benefit from a lower tax bill when they sell shares. Instead of being treated as income tax, employees' profits are taxed as capital gains, making the overall tax burden considerably lower.

The benefits of EMI schemes

As one of the most well-established employee equity strategies for UK startups, EMI schemes have a number of advantages for companies and for employees. Employees benefit from capital gains tax relief and there are corporation tax relief opportunities for employers too.

Compete for talent against larger companies with deeper pockets

EMI schemes are best suited to early stage startups that expect to grow exponentially within the next 10 years. To do that, these companies need to attract talented staff, but they’re unlikely to be able to compete with established competitors on salary and benefits. An EMI scheme, with its potential for a significant payout at a low tax rate, can improve the startup’s offering to future hires.

Equity is too often thought of as a ‘nice-to-have’ perk. EMI options can transform equity into a talent-drawing tool.

Incentivize and motivate your people

One of the main reasons companies give employees equity is to encourage them to focus on the long-term trajectory, not just their next paycheck. Equity has been shown to aid retention and motivation: in Ledgy's State of Equity report, we learned that employees who don't have share options would be more motivated if their company granted them an equity stake.

Qualifying conditions for an EMI scheme

Not all companies – and not all employees – qualify for EMI schemes.

Which companies qualify for EMI?

The UK Government & HM Revenue & Customs recently approved some significant increases to EMI plan limits, effective 6 April 2026. To be eligible for an enterprise management incentive scheme, qualifying companies must:

Have a UK permanent establishment. To establish this, your company must meet at least one of two requirements:

- Have a UK permanent establishment. To establish this, your company must meet at least one of two requirements:

- The company must have a fixed physical place of business in the UK where all or some of your company’s activity is conducted, such as an office, a branch, or a factory;

- Or, the company must have an agent who is authorised to act on your company’s behalf, and regularly exercises on this authority by entering into contracts.

- Have less than £120 million worth of gross assets (prior to 6 April 2026, this was £30 million).

- Have fewer than 500 full-time employees (prior to 6 April 2026, this was 250 FTEs). Part-time employees also contribute to that total, proportionally to their working time. For example, if a full-time employee works 37.5 hours a week, someone working 14 hours a week counts as two-fifths of an employee.

- Be independently owned, controlling more than 50% of its ordinary share capital.

- Not perform certain 'excluded activities', including banking, farming, legal services, and property development.

The employment-related securities filing deadline for UK companies is 6th July. Companies must submit an ERS report whether or not there have been new transactions in your equity schemes. Get started on gov.uk.

Which employees qualify?

To be eligible for EMI options, each qualifying employee must:

- Work in the business for 25 hours a week, or spend at least 75% of their working time in the business. For example, if an employee works four hours a day four days a week, they can qualify for a company’s EMI scheme if they spend at least 12 of those 16 total hours working for that company.

- Not control 30% or more of the company, alone or with an associate.

How EMI options work: valuations and strike prices

Under EMI scheme rules, companies don’t grant shares immediately. Instead, employees are granted the option to buy shares at some point in the future, at a fixed price.

This price — known as the strike price — is based on the shares’ value at the date of grant. Companies usually base the price on the actual market value (AMV) of the shares, meaning how much the shares are worth minus certain restrictions. The AMV is slightly lower than the unrestricted market value (UMV), which, as the name implies, ignores those restrictions. It’s important that you use the lower price, as it can increase the return your employees make later.

Companies setting up an EMI scheme must submit a valuation assessment that is mutually agreed by the company together with HM Revenue & Customs (HMRC). At that point, you have 120 days to grant the options.

The company establishes when employees will be able to exercise their options – i.e., buy their shares at the strike price – by creating exercise windows, which usually arrive at a liquidity event such as a public listing or potentially an acquisition. Under EMI schemes, employees normally have 10 years from the grant of the option to exercise their options to buy their shares. As of 6 April 2026, this 10 year limit can be extended to 15 years for existing unexercised options.

Unlike share schemes that haven’t been approved by HMRC, your employee will be able to keep most of that value, without losing a significant chunk to taxes. Your company also gets to claim a tax deduction on the difference between the price the shares were granted at, and their exercise price.

EMI: just one of four HMRC-approved share schemes

Some share schemes are approved by HMRC, and others aren’t. Founders looking to maximize flexibility can give shares to their employees independently of HMRC. Unapproved schemes have no restrictions on asset worth, company size, contract type or strike price, for example. You also don’t need to have company valuations approved by HMRC.

However, your employees will not receive any of the tax benefits associated with EMI or other approved schemes. They will have to pay tax on the difference between the strike price and the price at exercise, in addition to CGT at the full 20% when they sell the shares.

HMRC backs four types of employee share schemes, including EMI. Employees who are granted shares through these schemes can all benefit from reduced taxes, but some schemes may be more appropriate for different companies.

In addition to EMI, other HMRC-approved employee share schemes include:

- Save As You Earn (SAYE). Employees are granted share options at up to 20% below then-market value. Over three to five years, they contribute between £5 to £500 of their salary every month to a savings scheme. At the end of the contract, they can exchange the savings for shares at the discounted rate, and potentially receive interest on the savings. The company must make SAYE schemes available to all qualifying employees.

- Share Incentive Plans (SIPs). Employees acquire shares directly, and don’t have to pay income tax or National Insurance on the value if they keep the shares in the plan for five years. Employees can spend a limited amount of their pre-tax salaries on so-called partnership shares, which employers can match up to a certain amount. The employer can also give each employee up to £3,600 of free shares in a tax year. Employees can reinvest dividends received on free or partnership shares into more shares (called dividend shares). SIPs must be available to all qualifying employees.

- Company Share Option Plan (CSOP). CSOPs are similar to EMIs, in that the employer grants market value share options to be exercised at a later date, with no tax paid on the difference, and can be offered to just certain chosen employees. However, the market value of the shares granted to each employee must be less than £60,000. Under a CSOP, employees typically have to wait at least three years between when the shares are granted and when they can exercise them, whereas EMIs can potentially vest immediately. Unlike EMIs, CSOP schemes have no limit on company size.

All of these schemes enable employees to acquire shares and hopefully reap financial benefits, without paying income tax and National Insurance. However, EMIs have the potential to deliver significantly larger returns, because there’s a higher cap on the available shares.

Under an EMI, the market value of the shares each employee can be granted is £250,000 over three years, compared to £60,000 a year under a CSOP, £500 a month under a SAYE, or £3,600 per tax year under a SIP free share award.

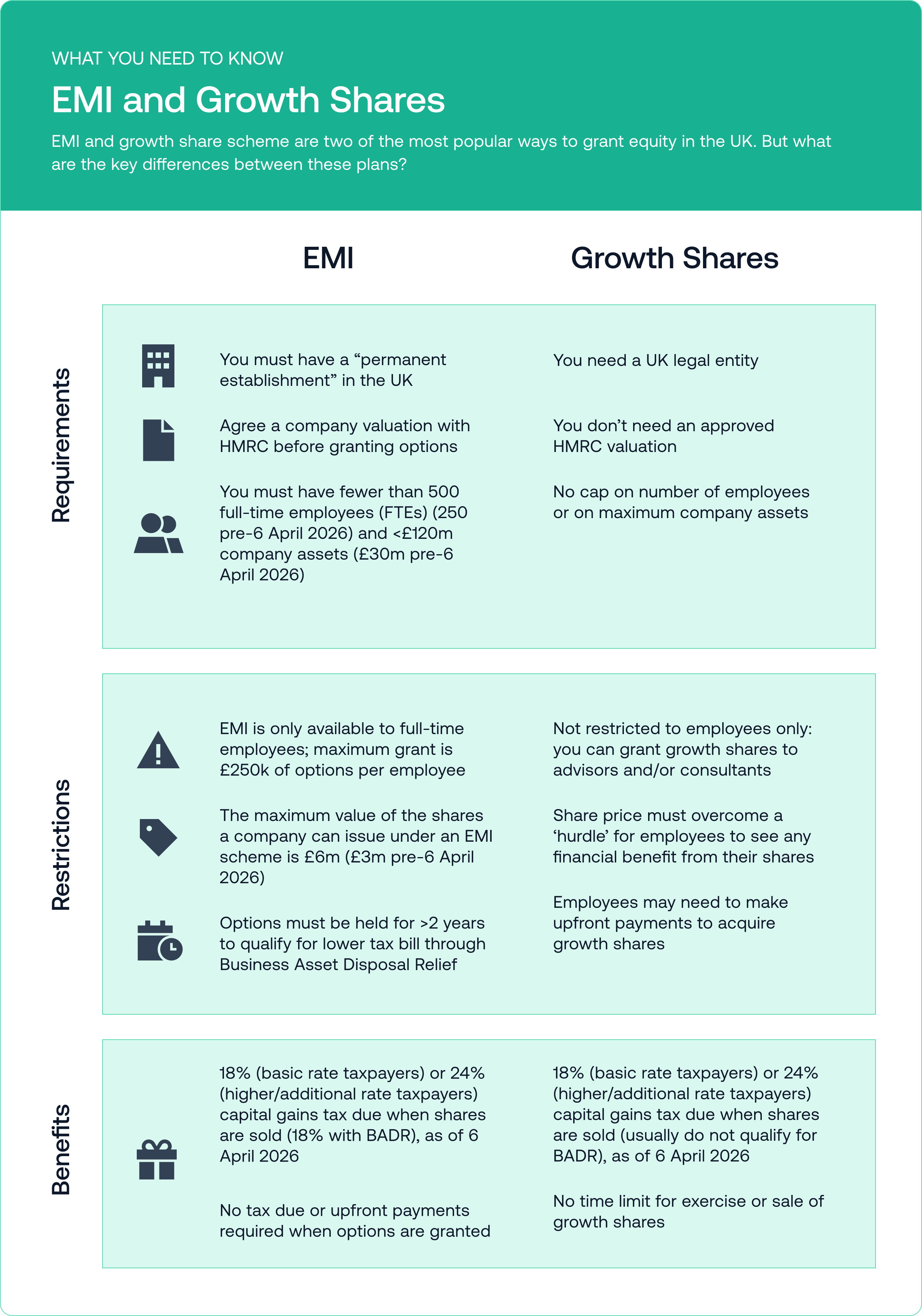

EMI vs growth shares

There are also methods of setting up and scaling an employee equity scheme that don't need approval from HMRC. Many companies use growth shares to distribute equity to the team without having to jump through the regulatory hoops required to set up EMIs. Here are a few key differences between enterprise management incentives and growth shares.

UK base

To set up an EMI plan, companies only need a "permanent establishment" in the UK. To qualify for a growth share scheme, on the other hand, companies need a UK legal entity.

Restrictions

While EMI share options are restricted to employees only, it's possible to grant growth shares to advisors and consultants as well as full-time team members.

Because EMI share options are limited to companies with under £120 million in assets and fewer than 500 employees, EMI is better suited for companies at an earlier stage of development. Growth shares don't have these limits, so can be used by more mature businesses.

Taxation

There is no tax due when employees exercise their EMI options. In some circumstances, though, employees may need to make an upfront payment when buying growth shares.

The capital gains tax payable when growth shares are sold is 24%, but as long as EMI options are held for over two years employees may be eligible for business asset disposal relief, which can reduce their EMI tax bill to 18% (wef 6 April 2026). Generally speaking, EMIs are the most tax efficient option for companies and employees.

Still unsure which option is right for your company? This graphic lays it out clearly for you:

How to set up an EMI scheme

The UK government has made EMI schemes relatively easy to set up. Once your company has established a permanent UK base, and your legal and financial advisors have confirmed that your company meets the other eligibility requirements for the EMI, the next steps are:

- Outline your scheme. Determine which of your employees should be included in the scheme, plus the vesting schedule for their share options. Will the options be exercised based on an exit or liquidity event? Or simply after a certain time period has elapsed? whether the options will vest based on an exit; the condition of meeting certain goals; or after a certain time period (within 10 years of granting, or 15 years if you choose to extend the exercise period and modify your scheme rules accordingly).

- Calculate an internal valuation. Have accounting professionals compile an internal report that establishes AMV and UMV.

- File your valuation with HMRC. Send your internal valuation and a completed VAL231 form to HMRC. This can help ensure your employees are granted options at the correct price to get the tax benefits.

- Hit your deadline for granting, and get board approval. You have 90 days to grant your options from the date of HMRC’s letter confirming the valuation and strike price. During this time, you need to confirm the employee share pool – the number of shares you'll keep aside for employees. You also need to have your board and existing shareholders approve your plans.

- Grant the options. Once you have approval, you can grant your team's EMI options. Make sure your employees understand the details of your EMI scheme, and have access to someone who can answer their questions.

- Register the scheme. Once you’ve granted the EMI options, you have 92 days to register the scheme and the options you’ve granted with HMRC.

Your EMI deadlines

There are several key deadlines companies deploying an EMI scheme must meet, to ensure their employees receive the tax benefits.

Ledgy makes it easier to keep track of these key dates, and to monitor the progress of the vesting period (the time between when the options are granted and when they can be exercised).

- Once HMRC has confirmed the valuation and the strike price, the company has 120 days from the date of the confirmation letter to grant the options at that price. (This was changed from 90 days as a response to COVID.)

- From April 2027, the company will no longer have to notify HMRC within 92 days of the date on which options are granted. Until then, companies are still required to notify HMRC of options granted within 92 days. Companies can generate a prefilled EMI option grant notification form from the Ledgy platform.

- In the instance of a disqualifying event, employees must exercise their options within 90 days to still benefit from Entrepreneurs’ Relief, which reduces Capital Gains Tax (CGT) to 10%. If the employee misses this 90-day deadline, they will have to pay income tax and possibly National Insurance on any value the shares gain between the date of the disqualifying event and the date of exercise.

- The UK government website states that for any grants made in a given calendar year, "you must tell HMRC [...] on or before 6 July following the end of the tax year in which the grant is made." This is the annual scheme return requirement.

Once your EMI scheme is live, put these dates in your calendar – don’t fall foul of a technicality when your employees’ equity is concerned, as you and your employees could lose access to the benefits of the EMI scheme.

{{callout-2}}

EMI top tips

Here are three recommended best practices to make sure your EMI scheme runs smoothly.

Communicate with your employees

Neither your company nor your employees can reap the full benefits of EMI share option schemes if people don’t know how the scheme works and how to make sense of share ownership. Read Ledgy's guide to explaining equity to your team to get you started here.

Consult professionals

Although enterprise management incentives are designed to be as user-friendly as possible, there are still loopholes that can trip you up. To make sure you’re ticking all the necessary boxes for your company, consult with equity specialists in finance and law.

Keep on top of your deadlines

One of the biggest mistakes startups make when executing EMI options schemes is missing deadlines set by HMRC. This can disqualify your employees from the tax benefits they should receive under an EMI scheme. Luckily, you can handle EMI notifications and annual return reporting right in the Ledgy app:

%20(1).png)

Conclusion: for the right companies, EMI can be transformative

The UK government created enterprise management incentives to help UK-based startups attract the best talent in their respective industries. Sharing equity in your company gives potential hires a reason to choose you, and engages your team on a deeper level as together you build something special.

Interested in learning more about managing equity as you grow? Learn how UK scaleup Audiomob manages an EMI scheme on Ledgy.

Frequently Asked Questions

What are some key EMI reporting deadlines to look out for?

How do I manage my EMI scheme with custom software?

Stay up to date! 🎉

Subscribe to our newsletter and receive the latest insights on the equity world

Automate your Equity Planning

Use Ledgy for bulk document creation and digital signature facilities for all international grant types in a centralised platform.

Find out how

.png)