Companies thinking about setting up a share scheme in the United Kingdom have many options to choose from. Company share option plans (CSOP) have undergone recent changes, so what's the impact on companies and their people? Come with us as we take you through the ins and outs of CSOPs.

What is a company share option plan (CSOP)?

A company share option plan (CSOP) is a type of share scheme for companies operating in the UK. It allows companies to grant share options to employees with both parties benefiting from different forms of tax relief.

A company share option plan needs to be registered with HM Revenue and Customs, the UK's tax authority. The market value of new grants under a CSOP also needs to be agreed with HMRC. As outlined by HMRC, the process for agreeing a CSOP valuation is:

To agree a market value for your shares, write to [our Shares and Assets Valuations team] and include:

- a proposed value for your shares

- 3 years of accounts before the valuation date, or if the company is newly trading, any accounts available at the valuation date

- any other information that might be relevant (for example, plans to sell or float the business)

But CSOPs are only one of the UK's four government-approved share schemes. The other three are:

- Enterprise Management Incentives (EMIs)

- Save As You Earn (SAYE)

- Share Incentive Plans (SIPs)

Let's compare CSOPs against EMIs, the leading share scheme for scaling companies, in some more detail.

CSOPs vs Enterprise Management Incentive plans

Enterprise Management Incentives (EMIs) are still the most popular way to grant equity in earlier-stage UK startups. But there are also some compelling reasons to think about CSOPs for your company. Here are a couple of the key differences between the schemes.

The value of people's equity

Of the government-approved share schemes, EMIs have the most generous allocations per employee: each individual can be awarded a maximum of £250,000 worth of equity in the company. Under CSOPs, this total is lower: participants in the plan can be awarded £60,000. (However, this limit has doubled from £30,000 in recent months – see below for more info.)

Scheme limits

EMI schemes are designed for early-stage companies, and their upper limits often prompt companies to explore other share scheme types once they reach a certain size and scale. For instance, companies starting EMI schemes must have fewer than 250 full-time employees, and under £30 million in gross assets. Unlike EMIs, CSOPs have no upper limit on company headcount or assets.

Remember, companies can operate multiple share schemes simultaneously: many companies transition from EMIs to a growth share scheme or CSOPs once they've reached the upper limits of the EMI scheme. However, running multiple plans without tailor-made software can place a significant burden on internal teams. Ledgy makes equity work by automating many of the time-consuming processes that go into running an equity plan.

2023 changes to CSOPs

Earlier in 2023, the UK government made significant changes to CSOPs. The changes focused on the share option limit for each employee, and the nature of share classes CSOPs can be established as. nature of the share classes into which companies should fold CSOPs.

First, the value of the shares granted to each employee is limited to £60,000 – a significant increase from the £30,000 maximum value previously in place.

Secondly, the 'worth having' clause has been removed. Previously, CSOP shares had to be granted in a share class that was either broadly held by people other than employees or directors, or in a share class that gave employees and directors effective control of the company. With this clause removed, it is easier for companies to be flexible in allocating CSOPs to the right share class for the business.

The result of these two changes is that since 2023, the average company share option plan has become more powerful and potentially able to deliver better returns for the employees that hold CSOP options and/or shares.

Which companies and employees are eligible for CSOP schemes?

CSOPs are highly flexible, and almost any company can apply through HMRC to set up a CSOP, with self-certification making the process simple. When it comes to employees, CSOPs can be granted to any employee or full-time director (meaning a director who spends more than 25 hours per week working on company business).

CSOP tax advantages and treatment

When issued in a compliant manner, CSOPs offer significant tax relief for employees and businesses.

There is no income tax or national insurance contributions payable when CSOP shares are granted or when exercised, as long as team members wait three years to exercise their options from the date they're granted. (CSOP options usually have a 10-year lifespan.)

Capital gains tax

When employees sell their CSOP shares, employees don't need to pay income tax and only need to pay capital gains tax on the gains above the exercise price as long as they've held their shares for three years after the grant date. Like other share schemes, CSOPs also have an annual capital gains tax exemption which is £6,000 in the 2023/24 tax year. That means the first £6,000 of gains for employees will be free of capital gains tax.

Companies/corporation tax

Companies also qualify for a corporation tax deduction relating to any accounting period in which options are exercised. As long as CSOP options are held for at least three years, the company will also have no national insurance contributions to pay.

CSOPs: other key facts

Let's quickly break down what else companies and employees need to know about CSOPs.

- Companies can grant CSOP options to team members at any size or stage, including if the company is publicly listed.

- A CSOP is a discretionary plan: this means founders and directors can select who to include in the share scheme. This stands in contrast to all-employee share schemes like SIPs, where companies have to give equity to every team member.

- It's possible for CSOP awards to be contingent on performance conditions. This can be a benefit for the employer as it means people qualify for their CSOP ownership stakes when they have added significant value to the business over time.

- Like other types of share plan, CSOP options vest over time. Many companies' share options vest over four years with a 12-month cliff. In Ledgy's 2023 State of Equity and Ownership report, we learned that a majority of companies in four key markets – the UK, US, France and Germany – all use this standard vesting schedule.

Is a CSOP right for you?

Particularly since the UK government's enhancements to the CSOP share scheme in 2023, CSOPs have become a useful tool for companies seeking to grant equity to employees on a discretionary basis.

In particular, companies outgrowing their EMI schemes should look at CSOPs alongside other unapproved share schemes like growth shares, which aren't restricted by company size and number of employees.

FAQs

Are CSOPs limited to UK companies?

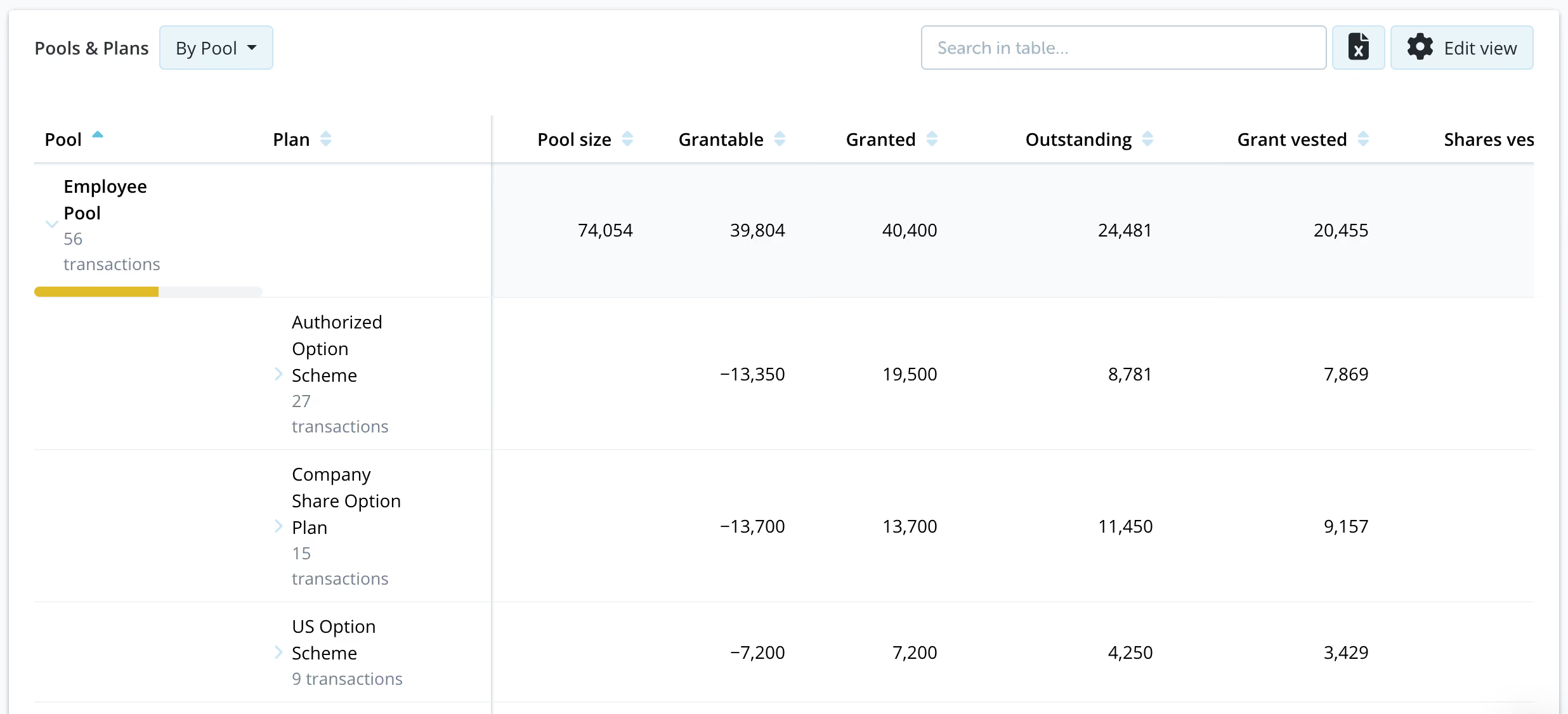

CSOPs are principally designed for companies with a UK entity, but US companies with a UK presence may be able to set up a company share option plan. Below is an example of an employee equity pool on Ledgy, showing how a company share option plan can sit alongside a US option scheme:

US companies interested in setting up a company share option plan should consult a lawyer or accountant to see if they could be eligible.

Stay up to date! 🎉

Subscribe to our newsletter and receive the latest insights on the equity world

Automate your Equity Planning

Use Ledgy for bulk document creation and digital signature facilities for all international grant types in a centralised platform.

Find out how

.avif)