Introduction

Equity is a powerful compensation tool. It helps companies attract and retain top talent and, in return, can deliver game-changing financial outcomes for employees. But do the benefits for companies and employees outweigh the costs?

One of the key components of this equation is tax. For companies, taxes present an administrative burden - it takes time and effort to comply with them and take each employee’s specific situation into account. For employees, the actual cost of the tax payment must be considered. So it’s no surprise that employees and companies often have many questions about equity and taxes. When is my next filing deadline? How much will be due? When and how much does the company withhold in taxes? When is it worth it for employees to exercise or sell?

And the answer is… It’s complicated. Tax arrangements depend on the jurisdiction, the type of share award or scheme in use, the different events in the lifecycle of the award, and the employee’s situation. Tax handled incorrectly can also have great consequences for both companies and employees, from underpayment or overpayment of tax through to compliance penalties.

In the UK, publicly listed companies can choose from a wide range of award types including save as you earn (SAYE) schemes and share incentive plans (SIPs), RSUs, ESPPs, unapproved options and more. So how does a company even begin to navigate this complexity?

What taxes are different plan types subject to and when?

For publicly listed companies in the UK, three main taxes apply to equity compensation: income tax, employee and employer social contributions tax, and capital gains tax.

Generally, the realisation of an equity-based award is subject to income tax up to a maximum rate of 45%, depending on the participants’ individual circumstances. The tax point may vary depending on the award type. In publicly listed UK companies, income tax is withheld by the company.

The rate of employee and employer social security contributions depends on the employee’s earnings, including earnings from the taxable event according to the award type and the employee’s regular salary. These are known as ‘National Insurance Contributions (NICs)’ in the UK and are paid by both the employer and the employee. For employees whose earnings from the taxable event and regular salary are below the “upper earnings limit”, the capped employee NICs of 8% is applied and withheld by the company. If a person’s earnings from the taxable event and regular salary are above this limit, then an additional employee NIC of 2% is withheld by the company. In addition, there will be employer NICs at 13.8% which is payable by the employer and is uncapped. It is possible in the UK for the employer NICs to be passed to the employee.

Capital gains tax (CGT) in the UK is currently 20% for higher-rate taxpayers. It is anticipated that changes may be made to this rate following the Autumn 2024 budget. Generally, CGT applies to any profit an employee makes if they sell their shares at a price higher than the share price at the time they acquired the shares. CGT is payable by the participant after filing their annual tax returns. Tax residents in the UK have an annual capital gains allowance which can be used against gains. This is a specific amount of capital gains up to which CGT is not owed and only gains made on top of that are taxable.

Let’s break down the different share plans in the UK and how taxes may apply to them.

Share option plans

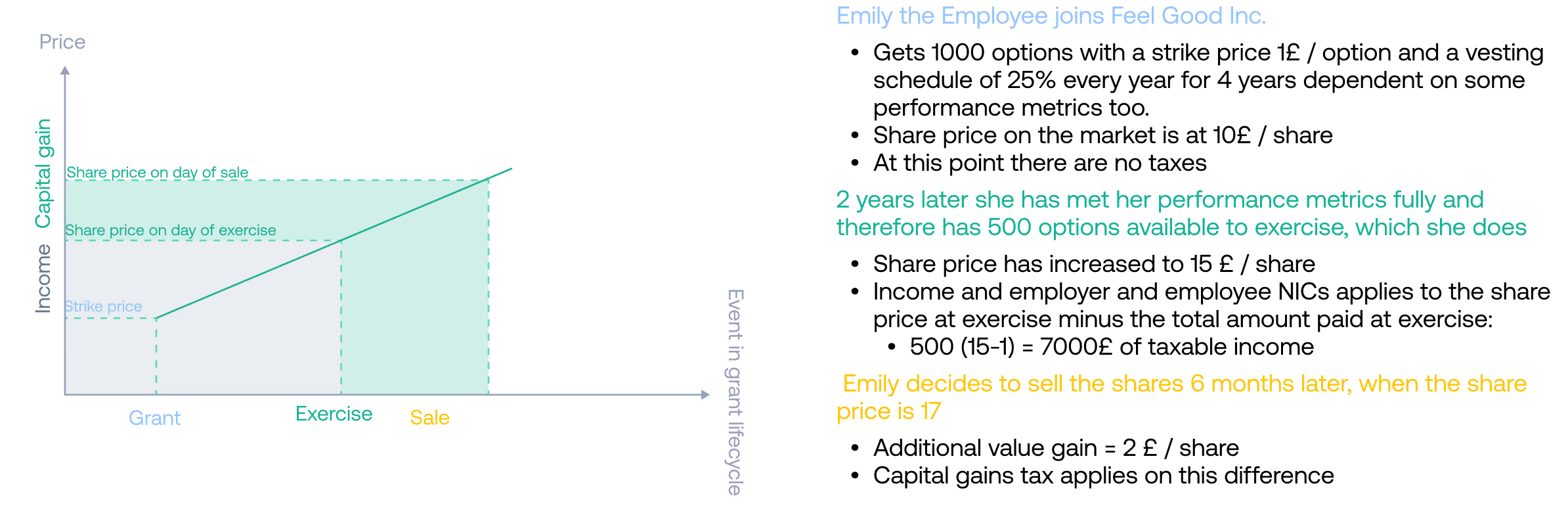

Share options give participants the option to buy shares offered by the company at a predetermined (often more favorable) strike price.

Taxable events are at exercise and sale, with income and employee and employer NICs applied at exercise, and capital gains tax applied at sale. The parameters of the award that influence tax amount are: the strike price, the market price of the shares at the time of exercise, and the sale price.

RSUs

Restricted stock units (RSUs) are a promise from the company to release shares to the participant once vesting conditions are met.

Taxable events are at vesting and sale, with income and employee and employer NICs applied at vesting, and capital gains tax applied at sale. The parameters of the award that influence tax amount are the market price of the share at the time of vesting release and the sale price.

ESPPs

Employee Share Purchase Plans (ESSPs) let participants buy shares in the company at a discounted price during a specific offering period. Pursuant to this style of ESPP, common in the US, the taxable events are generally at the point of purchase and sale. The parameters of the award that influence tax amount are the purchase price, market price on the day of purchase, and sale price.

In the UK, ESPPs may be structured as a savings arrangement with the right for the employee to buy shares at a discounted price in the future using accumulated contributions. This is to deter unattractive tax charges on the acquisition of the shares until the time of exercise.

ESPPs also may be structured as an “approved” plan in specific countries which provides tax advantages if certain criteria are met, such as a SIP or a SAYE in the UK as described below.

UK SIP

UK Share Incentive Plans (SIPs) are a government-approved share scheme that can provide tax advantages to employees. Different types of shares can be awarded under a SIP: Free shares, Partnership shares, Dividend shares, and Matching shares and these are held on behalf of employees in a SIP trust.

The timing of the withdrawal of SIP affects the tax treatment. If the shares are held for more than 5 years, there is no income or social contributions tax on their value. If the shares are sold, CGT may apply. CGT may not apply or be deferred when shares are transferred directly from the SIP into an individual savings account or personal pension.

UK SAYE

UK Save As You Earn schemes are savings-related schemes where participants can buy shares from their savings at a fixed price.

There is no income or social contributions tax. CGT may apply at the point of sale on the difference between the fixed price it was bought for and the sale price. It does not apply if the shares are transferred into an individual savings account within 90 days, or transferred to a pension directly from the scheme when it ends.

SIP and SAYE plans provide many benefits to employees, but they are complex and advice is required before their set up.

Summary table UK:

How to cover the tax due?

Income taxes and employee NICs are withheld by the company, meaning that the burden of reporting and paying the tax directly to the authorities is for the employer company. The company is therefore responsible for tracking, reporting and paying the correct amount of taxes withheld to authorities, paying the correct wage to the employee, and informing the employee about this in their payslips and tax forms. This is largely a challenge covered by the payroll department.

“Standard practice is to withhold the maximum rate for each employee. The one thing you don’t want to do is under-withhold” says Dave Quick. Payroll therefore withholds the maximum tax rate for all employees and then makes individual adjustments for each employee based on their situation if and when they are needed.

To cover these withholding taxes, employees and companies have different options: cash settlement, sell-to-cover, and net settlement.

With cash settlement, the amount due is withheld by the company from the employee’s regular wages. While this may seem like the most straightforward option, it is actually the most rare.

As monthly salary may not be sufficient to cover these liabilities (or employees may not want all or a large portion of their monthly salary used up in this manner), it is typical to offer employees the option to sell a portion of the shares from their award to cover the withholding taxes (and strike price, where applicable). This is called ‘sell-to-cover’ and means no actual cash is withheld from the employee’s regular wages to cover tax.

An alternative to this approach is called ‘net settlement’ whereby the employee receives a reduced number of shares, calculated as equal to the net value the employee enjoys after withholding taxes (and strike price, where relevant) plus a cash amount equal to the taxes and strike price (where relevant). The company will then pay the relevant withholding taxes to the tax authorities from the cash amount.

In each case outlined above, the withholding taxes will be the same, it is just the method by which these are satisfied that alters. These methods are applicable only to the withholding tax and not capital gains tax which is payable by the employee after filing their yearly tax returns.

Following the example of stock options, let’s assume an employee exercised 500 options with a strike price of £1 / per share and a market price of £15 / per share. The taxable income is £7000.

It is assumed that the option holder’s marginal tax rate is 45% (such that all their gain would be taxed at 45%). As the option holder is an additional rate taxpayer, their employee NICs would have exceeded the upper earnings limit, therefore the taxable gain would result in employee NICs at 2%. It is also assumed that the employer NICs have not been passed to the option holder. Broadly, the income tax and NICs arising on the exercise of the options would be:

Income tax: £3,150 = £7000*0.45

Employee NICs: £140 = £7000*0.02

Total: £3,290

For completeness, the company would also be required to pay employer NICs at 13.8% (uncapped) and Apprenticeship Levy at 0.5% (if their UK pay bill exceeds £3 million).

In order to cover this tax, the employee can:

{{info-box-1}}

Reporting obligations: What needs to be tracked and reported when?

Equity and its taxable events must be tracked meticulously including new grants made, vesting, exercising, sales and the prices relating to these. These all inform the withholding tax calculations and filings that need to be made to HMRC regarding payroll, employment-related securities, and employee tax forms.

Company filings

Payroll departments in UK companies have the responsibility to make the correct withholding tax considerations as they calculate and pay wages to employees, report, and pay the correct amount of taxes withheld to authorities, and inform the employee about this in their payslips and tax forms.

Payroll information must be reported to HMRC through Real Time Information (RTI) providing updated income tax and National Insurance information on or before the day payroll is run. Companies must then pay the amount due through the PAYE (Pay As You Earn) system to HMRC, by the 22nd of the following month. Companies must also keep payroll records to show that reporting has been done accurately for three years from the end of the tax year they relate to.

UK companies also need to report annually to HMRC about employment-related securities (ERS). Before being able to report on share schemes, companies must register them with HMRC. Annual reports include details about each scheme like new grants and acquisition of shares or other securities. Even if no reportable events have occurred, a “nil” return must still be made. The deadline for these reports is July 6th. Ledgy provides instant one-click downloads of ERS reports to make meeting this deadline hassle-free.

For each of these, there are penalties for late filings. It is also possible that tax advantages related to approved schemes are lost due to late ERS filings.

Employee filings

If an employee benefits from a gain subject to CGT, this needs to be reported in their annual Self-Assessment tax returns in the tax year in which the gain arose. There may be an annual exemption available. Companies must provide employees with the information they need for their tax forms.

Tax for a global workforce: What happens then?

Companies in the UK today almost always have a global workforce, meaning that a portion of their employees reside in countries outside of the UK. For them, the applicable tax rates differ from the rates covered above. “It is fairly simple and straightforward, you just have to know the differences between the tax rules applicable in the UK and in other jurisdictions.” says Dave. An example could be Germany where virtual share options are most common, however the introduction of the Future Financing Act may impact the rules around tax for employees in your business.

But what about employees who move jurisdictions during the duration of the grant’s life? A mobile workforce adds a whole other layer of complexity. “The broad principle is apportionment meaning that the taxes that apply are directly linked to the proportion of the time spent in a certain jurisdiction over the entire lifecycle of the grant.” says Dave. “General advice for mobility-related compliance is to ensure minimal risk especially for the higher earners in the organisation. Fines for non-compliance are often proportional to the earnings, so it’s really a question of scale. Make sure the ‘big fish’ are covered first.”

Getting tax efficient and compliant

Numerous countries provide tax-efficient plan structures that help companies minimise their administrative burden and employees to save on tax. “While there may be tax-efficient structures available in numerous jurisdictions, it generally makes sense to prioritise the “home” country in terms of the overall plan.” says Dave.

UK companies have numerous tax-advantaged plans available. For UK public companies the most important ones are: SIP (Share Incentive Plans), SAYE (Save as You Earn). SIP is a flexible and great option for participants as it has no income or social contributions tax. SAYE allows employees at all levels to invest in their company’s shares in a tax efficient way. “It is important for companies to take a realistic and practical approach, as it will likely be impossible to ‘mirror’ UK tax advantages in other jurisdictions. It is less easy for listed companies to use tax-advantaged schemes internationally. It is nonetheless worth checking, especially if there is a large number of employees in a certain jurisdiction.” says Dave.

Both global and mobile workforces mean companies have to keep up with ever changing tax regulations in different countries to make sure they comply.

“Working in direct partnership with share plans experts at CMS, ShareReporter keeps up with evolving tax regulations in over 90 countries, and makes them accessible to companies at the click of a button. Combine that with Ledgy’s ability to track employee grants and which jurisdictions apply to which employee and you are definitely on the way to getting equity compliance right.” – Dave Quick, ShareReporter

While tax compliance can seem like a daunting task for companies of any size, there are tools and experts to help manage this. The most important thing is to get started right away. “Don’t put your head in the sand. It’s better to get compliant as soon as possible, even if in retrospect.” says Dave.

To learn more about how Ledgy and ShareReporter can help, go to Ledgy.com/tax-and-compliance.

Disclaimer: The information in this article is for guidance only and does not constitute legal or tax advice. The information is correct as of 16 September 2024.

Ledgy’s settlement workflow allows employees to select from the methods above directly on the app. With one seamless workflow between employees, admins, and integrated trading partners, Ledgy allows companies to streamline the full settlement process. While employees benefit from a frictionless trading experience, admins can effectively keep track of the transactions and withholding methods allowing them to meet compliance and reporting obligations more easily down the line.