Germany is striving to become more startup-friendly. In 2023, the government introduced an important change to its tax laws, aiming to help more employees own a part of the companies they work for through employee equity plans. The new Future Financing Act (Zukunftsfinanzierungsgesetz, or ZuFinG for short) has come into force as of late 2023/early 2024. The government hopes that the introduction of the Future Financing Act will make it easier and more attractive for employees to hold equity in their companies, which is something that not only benefits workers but also helps companies stand out and compete internationally.

The Future Financing Act or Zukunftsfinanzierungsgesetz, led to several tax changes meant to encourage a culture where employees owning a part of their company became the norm in Germany. Why does this matter? Employees owning shares are more likely to be engaged with the company's success. Companies with employee shareholders tend to do better because these employees are working not just for a paycheck but also for the success of their investment.

Employee ownership is especially crucial for startups. In the early stages, when money is tight, offering shares to employees can be an excellent way for startups to attract and keep top talent. However, equity is not just for new companies. Established businesses can use it, too, and offering an ownership stake can help to make the company more attractive as a place to work.

Even with the changes made in 2021’s Fund Location Act, Germany's rules for employee ownership were not as good as they could be, especially in comparison to other countries. The Not Optional initiative, which ranks more than 20 countries in Europe and beyond in their approach to awarding equity, judges Germany’s treatment of stock options as among the least attractive or efficient.

{{quote-1}}

Employee Share Ownership in Germany before the Future Financing Act (ZuFinG)

Now, let's dive into how Germany's system works when it comes to employees receiving shares or ownership stakes in the company they work for. This part of the system is a bit technical, but it's crucial to understand the changes introduced by the Future Financing Act.

In Germany, if an employee receives a share in their employer's company either for free or at a discount, this is seen as a form of income from employment, according to the Income Tax Act (EStG). This is known as a "monetary advantage" or “benefit in kind”. It's a type of compensation that employers give to their employees, but it's not handed out as cash.

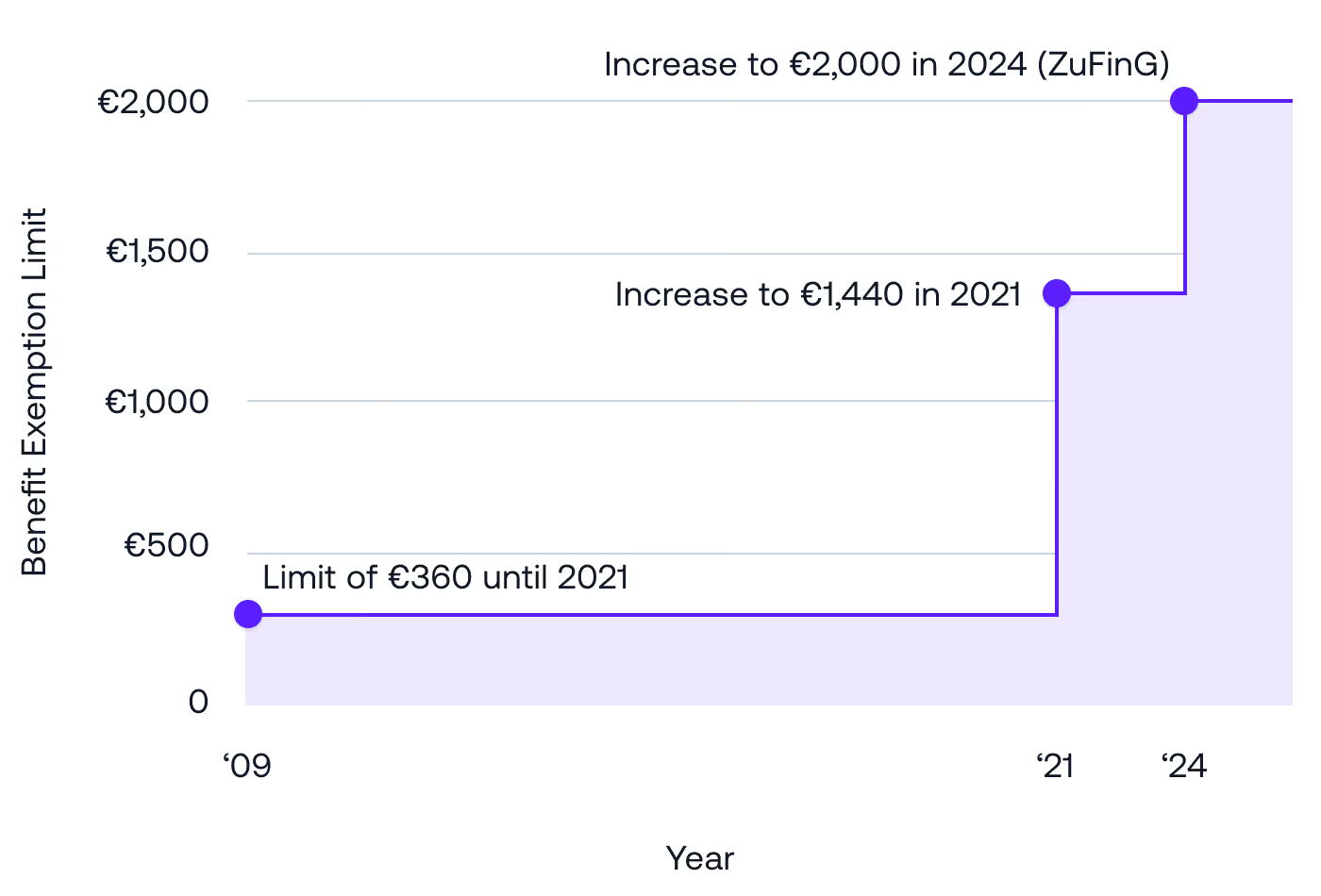

Before the enactment of the Future Financing Act, the EStG specified that these benefits could be tax-exempt up to €1,440. However, there was a catch: the offer to receive company shares must be available to all employees who have been with the company for at least a year without interruption. While the company can set different conditions for different employees (like how much they might need to pay to get these shares), the EStG stated that every employee with over a year’s service would need to receive an offer to participate in the scheme, otherwise there would be no exemptions available.

Moreover, if the benefit is not given on top of the base salary as an extra perk, but at the expense of existing wage items, the tax exemption would still hold but social security (which is around 20% for both the employer and employee) would become due. In other words, social security exemptions are only available for share benefits that sit ‘on top’ of the base salary.

Key Changes for Companies Under ZuFinG, The Future Financing ESOP Framework

The Future Financing Act (ZuFinG) makes it easier for more startups to use the possibility of deferred taxation to avoid “dry income”. The so-called “dry income problem”, is where a tax bill would be triggered if employees acquired shares for no cost or at a discount.

To qualify for these benefits, the employer company must generally be classified as a small or medium-sized enterprise (SME) according to EU law at the time of the equity transfer. Now, ZuFinG (the Future Financing Act) relaxes the criteria for eligibility by doubling the thresholds for turnover and balance sheet totals. Now, companies with an annual turnover of up to €100 million (previously €50 million) or a balance sheet total of up to €86 million (previously €43 million) can benefit from the tax advantages.

Several other qualification conditions are now significantly more lenient. Beforehand, only companies with fewer than 250 employees could qualify for the benefits; now, companies with fewer than 1,000 employees can qualify. Companies can qualify if they met the headcount and turnover or balance sheet criteria at any point in the last six years. Additionally, the previous legislation only accommodated companies under 12 years old. Now, Zukunftsfinanzierungsgesetz, (ZuFinG), allows companies established up to 20 years ago to grant employee ownership more easily.

Starting in the 2024 tax year, the tax exemption limit for benefits from receiving company shares at a reduced price or for free is increased to €2,000, up from €1,440. (A limit of €5,000 had been discussed while the bill was being drafted, but this did not make it into the ratified ZuFinG legislation.) This means employees can get a larger portion of their share ownership at preferential/discounted terms without paying taxes on it. The below chart tracks the exemption limit’s evolution over time:

However, any benefit in kind above €2,000 will still be taxable at individual progressive tax rates.

Furthermore, Zukunftsfinanzierungsgesetz extends the maximum deferral period for taxing these benefits from 12 to 15 years, even for shares transferred before 2024. Special considerations are made for 'leaver events,’ such as when an employee leaves the company and their shares are bought back, ensuring taxation is based on the actual buy-back value rather than market value.

Other elements that failed to make it through the drafting process included a ‘group clause’, which would have allowed employees of subsidiaries in groups of companies to participate, and a holding period that would have stipulated a minimum term of service to qualify employees for the benefit. Companies and employees should monitor further amendments to the ZuFinG legislation, which may bring enhancements to the group clause.

But while the increase in the tax exemption limit is welcome, it merely brings Germany closer to competitive parity with other jurisdictions rather than offering a significant advantage. On the other hand, the improved possibilities to defer taxation for real shareholdings in SMEs have generally been perceived as a good progress – at least according to the initial industry chatter around the Future Financing Act.

Which Companies are the Best Fit for New Employee Share Plans?

The Future Financing Act is shaking things up for companies – particularly startups and small- to medium-sized enterprises – interested in offering Employee Share Plans (ESPs). By introducing new rules, these companies can now tap into greater tax benefits for their employees, helping them bring top talent on board with share schemes.

Companies who are ready to walk the new path can offer their employees an upside that qualifies as capital gains, with minimal upfront investment required of employees. As a company, you need to be ready to deal with real shares – rather than virtual shares for a potentially broader population of employees. But it doesn’t have to be complex.

There are proven structures used in private equity portfolio companies for many years that cater for similar arrangements. There typically is a pooling vehicle (which can take the form of a ‘Kommanditgesellschaft’ partnership, or some form of nominee or trust arrangement) that eases administration while facilitating governance. This can give employees partnership interest, which can be transferred more easily (e.g. in leaver or new joiner cases) than shares in a German GmbH, for example.

Are VSOPs Still Relevant in Germany?

Despite the excitement over the potential of ZuFinG in Germany, the reality is that Virtual Share Option Plans (VSOPs) are still the most popular way for employees to benefit from their company’s success.

Although VSOPs do not grant actual ownership rights, they deliver some advantages for companies: for instance, they do not need to be bought back in leaver cases (exercising a call option) as they are forfeited by default. So why are VSOPs seen by many as unfit for purpose? Well, VSOPs will typically be taxed at progressive individual income tax rates up to 45%. Social security is also generally due on employment income (but this is currently capped in Germany at €90,600). For employees with salaries below this threshold, additional employer social contributions will also be due when cashing out equity held in a VSOP.

Unless cutting-edge equity management software tools are in use, having a large number of shareholders, especially in a typical German limited liability company (GmbH), can make the company less agile. As described above, pooling vehicles can help to mitigate the complexity for stakeholders managing equity plans, but these still need some ongoing care and maintenance. It will be interesting to observe how quickly ZuFinG helps ESPs take ‘market share’ from the incumbent VSOP structure that for now dominates in Germany.

Impact of New ES(O)P Rules on Germany's Tech Sector

The Future Financing Act is Germany's move to make its tech ecosystem more competitive, especially when it comes to offering real equity stakes (rather than virtual shares) to employees. The previous effort, the Fund Location Act of 2021, didn't quite hit the mark in getting employees more invested in their companies. The hope is that ZuFinG helps to fix this, especially by solving the dry-income problem and making it easier for companies to give real shares to their people.

This update comes at a crucial time. German startups and scaleups are finding it hard to attract and retain the best talent. Share-based incentive schemes are a way to attract exceptional people to the business, and Zukunftsfinanzierungsgesetz is a promising step to make Germany a more appealing place for tech professionals.

It is now key that advisors and providers support companies with actually implementing these new schemes, and help develop a proven and practical approach that can become the new standard. This should also mitigate companies’ fear of implementing an incentive plan that looks – at first glimpse – more difficult than a VSOP, which people are still familiar with despite its flaws.

With economic growth slowing down and Germany facing challenges like an aging population and a shortage of skilled workers, boosting entrepreneurial spirit among employees is more important than ever. The changes brought by ZuFinG are designed to help German startups grow, foster a sense of ownership among employees, and spur innovation. This is great news for local companies and gives international businesses an important supporting element when setting up shop in Germany.

Stay up to date! 🎉

Subscribe to our newsletter and receive the latest insights on the equity world

Cap Table Management Simplified!

Track transactions, model funding scenarios & manage real-time engagement with stakeholders all one platform with Ledgy.

Discover how